Over time, there are three things which have held true – death, taxes and a change in the global reserve currency.

By nature, all predecessors to the USD’s rule as the global reserve currency have fallen – brought down by a combination of declining geo-political influence, reduced economic power and a loss in confidence.

They have ranged from the Roman Denarius (250 B.C. – 200 A.D.), to more modern reserve currencies such as the Dutch Florin (1700’s), the United Kingdom’s Pound Sterling (early 1800’s – 1920’s) – all now succeeded by the United States Dollar (1920’s – present).

The post-World War I landscape, in which the USD entered as the de-facto global reserve currency, has changed dramatically and offers questions on how global monetary systems may operate in the future.

Today, I will take you through the history of the USD hegemony, an assessment of its health, and its potential successors.

Bretton Woods (1944-1971)

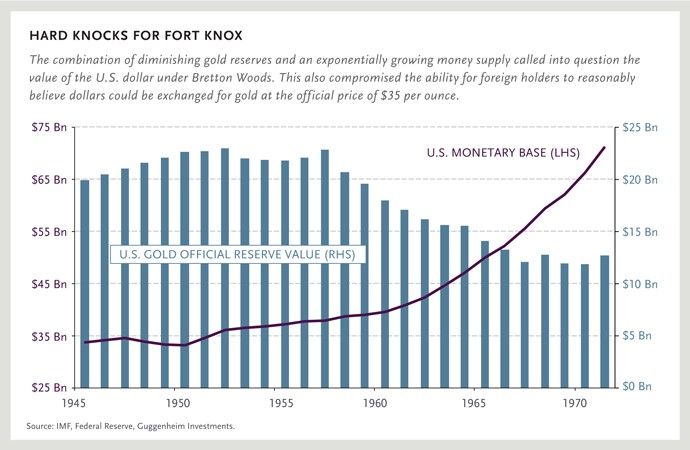

In 1944, the United States found itself as the largest custodian of gold – having accumulating reserves through seizure from its citizens during the Great Depression (to promote economic growth) and having received reserves as payment for weapons and supplies from countries entrenched in World War II.

These gold reserves, along with the USA’s position as the largest world economy eventuated in the establishment of the Bretton Woods system – where the USD would be backed by gold, and its allies would peg themselves to the USD (creating a gold peg by association).

This put the U.S in an unheralded position – acting as the sole monetary authority in a growing world economy.

However, the Bretton Woods system was flawed in its reliance on the U.S to maintain sufficient gold reserves to back the growing global economy.

As inflation began to rise due to rising demand, more and more of the USA’s trade partners asked to redeem USD for gold, reducing the value of the USD as the gold reserves which backed it dwindled.

This led to the cessation of the gold standard by President Nixon in 1971, subsequently bringing the Bretton Woods system to an end.

Petrodollar (1971-present)

With the gold standard abolished, governments around the world moved towards fiat currencies – whose value is driven only by governments mandating their use as a primary legal tender.

Current fiat-based monetary systems are built around the petrodollar system – where Saudi Arabia and other OPEC countries sell their oil exclusively in US dollars in exchange for U.S protection and co-operation. Therefore, any country who wants to buy oil from Saudi Arabia will be forced to use USD, which they can acquire either through receiving payments for exports in USD or exchanging their currency for them.

This process results in many non-oil producing nations selling exports in USD terms, creating consistent global demand for dollars.

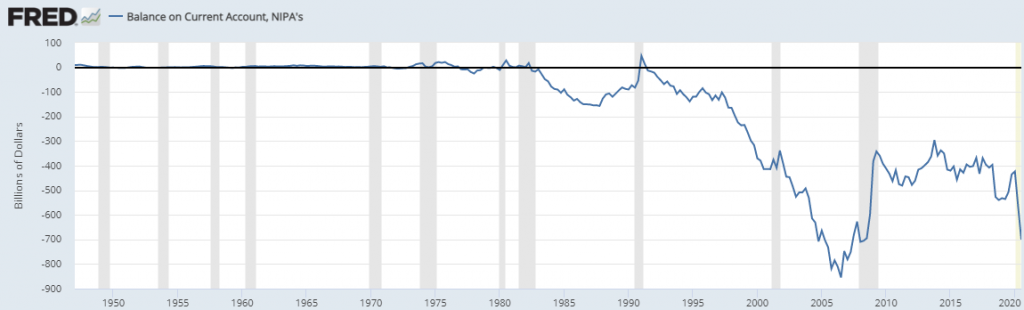

However, one’s status as a global reserve currency necessitates a consistent trade deficit.

Put simply, if you are the proprietor of the reserve currency, you will need to circulate cash to fund both your own economy, as well as the global economy.

As a result, you would need to have a net fund outflow (facilitated through having more imports than exports) – also referred to as a trade deficit, or current account deficit.

U.S Current Account Balance

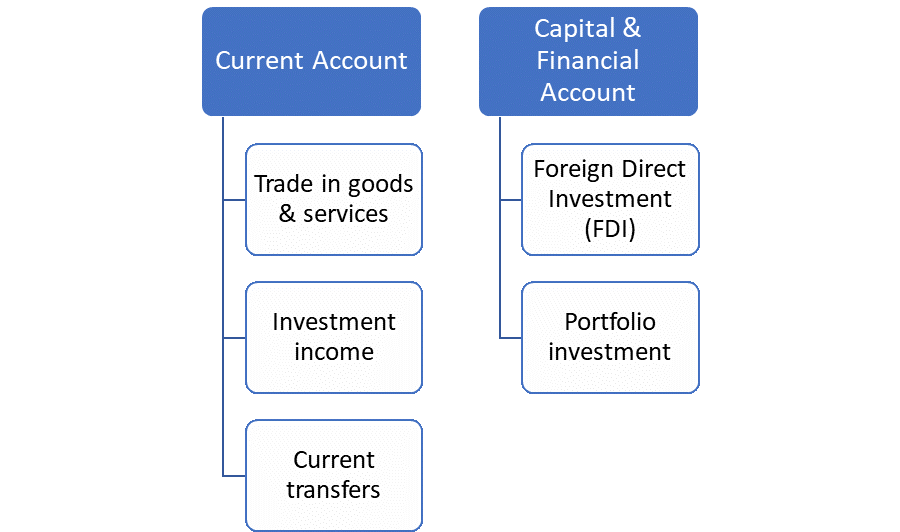

However, the presence of trade deficits also necessitates foreign debt, due to the need to achieve a “balance of payments”.

Again, put simply – if you have a net outflow of funds from trading goods and services, you need to bring balance to the equation by having a capital and financial account surplus – in the form of foreign investment. In the case of the USA, this involved the issuance of government treasury notes.

Whilst there are many benefits of being in control of the global reserve currency, there are also severe implications – outlined by the Triffin Dilemma.

Triffin Dilemma

The Triffin Dilemma was proposed by Robert Triffin to the U.S congress in 1960, exposing a fundamental issue with the Bretton Woods system. He stated that if the U.S were to stop running trade deficits, subsequently reducing the supply of US dollars to the global economy – economic growth would contract severely as a result of an appreciating U.S dollar and the resulting increased costs of any USD denominated trade.

This happened in the 1980s, where the USD rose for these reasons in relation to the Japanese yen and Deutsche mark, catalysing the need for the “Plaza Accord”, a joint agreement between France, West Germany, Japan, the UK and USA to depreciate the USD.

However, if the U.S continued to run trade deficits, the USD could erode in value if the return made on debt fell below its servicing costs.

Whilst the USD has enjoyed a further 60 years as the global reserve currency since Triffin’s prediction, much of this can be attributed to rapid global economic expansion and deflationary forces of debt, demographics and declining costs of technology.

However, as other global economies become relatively stronger (namely China), countries have sought to untangle themselves from the USD driven monetary system.

China and Russia have both led this change, with China paying for 33% of Russian imports in USD terms, down from 98% six years ago. Indian imports from Russia in USD terms have also declined from 100% to 20% in the same time span, holding great significance given the growing importance of China and India in the global economy, and the large proportion of which energy and commodities make up of Russia’s export base.

China has also undermined the existing petrodollar system through breaking the symbiotic relationship between the U.S and the global economy, by stopping the purchase of U.S Treasury’s and reducing existing reserves. This has forced the U.S to buy more of its own treasury’s when running fiscal deficits, having to intervene when there are shortages of creditors to the U.S highlighted through the repo market spike in 2019.

As time goes on, it is beginning to look increasingly likely that the USD’s position as a global reserve currency will weaken, which begs the question, what could take its place and what implications will this carry on financial markets?

Potential successors range from a continuation of fiat currency-based systems through either increasingly segmented monetary systems or a basket of currencies. Alternatively, we could go down the path of decentralised reserve assets such as cryptocurrencies – digital assets designed to work as mediums of exchange where ownership is stored in digital ledgers using strong cryptography to secure transactional details.

Segmented global monetary system

The global monetary system could continue to become more segmented, with countries electing to pay for less exports in USD.

This would be driven by decentralised energy pricing and looks most likely to eventuate should the USD lose its status as the global reserve currency. As previously mentioned, China and India have already begun to diversify the currencies used for the purchase of oil, with the trend likely to continue disseminating into other export markets as these countries look to reduce their dependence on the USD.

Baskets of currencies (Bancor)

As first proposed by John Maynard Keynes in 1940, the global reserve currency could materialise in the form of a basket of major currencies. As proposed, the currency (called Bancor) would only be used for international settlements and would be administered by a global central bank. By creating a basket of currencies, one would be able to avoid the negative implications of a country taking sole responsibility for being the global reserve currency.

Recent renditions of Keynes’ Bancor have included the Special Drawing Rights (SDR) implemented by the IMF post GFC, and the more recent Libra initiative proposed by Facebook.

Whilst both have been unsuccessful to date, the creation of Central Bank Digital Currencies (CBDC) could assist in providing a technological base for this to occur. However, in order for this to occur, and for the U.S to relinquish its position as the global reserve currency, we would require a much more stable and co-operative geopolitical landscape, which is looking increasingly unlikely as tensions continue to flare between China and the U.S.

Cryptocurrencies

The final alternative to the current U.S dollar hegemony is a cryptocurrency – with their decentralised properties having the potential to act as a neutral global reserve currency in an increasingly fractured world. The most prominent candidate would be Bitcoin – given its position as the largest and most well-known cryptocurrency, and its store of value properties, given its finite supply of 21 million Bitcoin.

Now, I know what most of you would be thinking – it’s too volatile, its unproven, it could be hacked (although incredibly unlikely in the future and impossible using existing technology) – but it remains as the main alternative which is immune to our current turbulent geopolitical landscape, and serves as the only alternative which could conceivably remain as a primary reserve asset indefinitely.

Whilst Bitcoin in its current form would be unsuitable, expansion of payments infrastructure and mass adoption could provide an opportunity for Bitcoin to act as the primary reserve asset of the world. However, the possibility of global implementation is unlikely, given the inability of central banks to manipulate the supplies and liquidity of Bitcoin.

Given the established nature of the global monetary system, it is likely that the USD will continue its role as the global reserve currency. However, it is important to consider what the world could look like without the USD as the global reserve currency, given the far-reaching impacts it would have both on investments, and life as we know it.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.