“Come on, come on, listen to the moneytalk”

ACDC (1990)

It has been a point of interest that Australian bond markets stick out in attractiveness compared to global peers, starting with our AAA-rated sovereign issued bonds, yielding higher than comparable AAA-rated peers (many of which have negative yields), and even higher than AA-rated peers such as USA, NZ and UK.

Then there’s the topic that our AUD has been performing quite well against other currencies.

An offshore investor who bought AUD bonds specifically to trade the currency differential have seen AUD/USD rally 27% from its low of 55c in March. And AUD can still be considered under-valued by traditional Purchasing Power Parity (PPP) methodology.

But where are AUD credit bonds, how are they faring?

The Australian domestic credit bond market is heavily weighted to financial services companies, with our 4 Major banks – ANZ, CBA, NAB, Westpac – dwarfing other issuers in size of bond issuance, accounting for upwards of 60% of the overall market.

For this reason, bond investors in Australia of any notable size will find they are naturally large holders of major bank paper.

However, there are many issuers – other banks, insurance companies, as well as the non-financial corporates such as BMW, Telstra, McDonalds, Pacific National, Woolworths etc. who finance large parts of their business operations via debt market issuance.

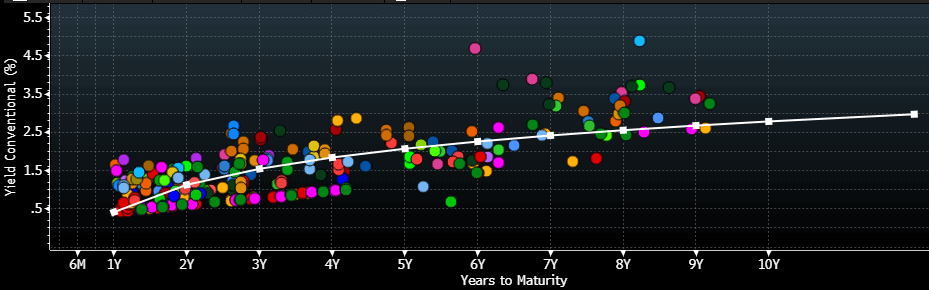

The following graphic represents the 70 different bond issuers in the AUD corporate bond complex, holding an investment-grade credit rating, issuing bonds 200mio AUD or larger.

Each colour represents a different issuer:

Source: Bloomberg

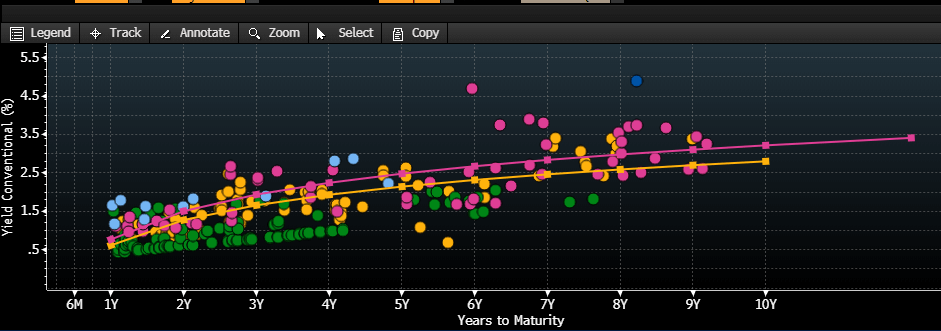

If I re-colour this graphic by credit rating rather than by individual corporate issuer, we can slice and dice the data to see what value certain securities offer compared to others.

Source: Bloomberg

In this sample, we can see that a 5y A-rated bond can offer a yield to maturity around 2.1%, while a BBB-rated bond offers similarly at 2.45%, compared to the ~1.2% yield on AA-rated bonds.

Central bank support

Herein lies the effect of central bank support. Are the AA-rated corporate bond issuers – mostly our Major bank’s bonds – worthy of such a large distinction between yields?

Well for one our major banks’ credit rating INCLUDES a credit for sovereign support – which was first applied during the GFC as part of the Rudd government’s explicit support during the crisis, later re-affirmed by the Turnbull government. Hence, our Major banks are AA rated as opposed to A rated, if they weren’t receiving this extra support that other debt issuers receive.

This is why there has been a flight to quality in credit these last 3-4 months, as investors seek higher-rated credit bonds to avoid price volatility.

Credit Rating Rotation

Credit bonds have latent equity beta, due to the influence of corporate earnings and profitability on default risk.

It is said that during good times credit bonds trade similarly to risk-free sovereign bonds, but during crisis trade more similarly to equities.

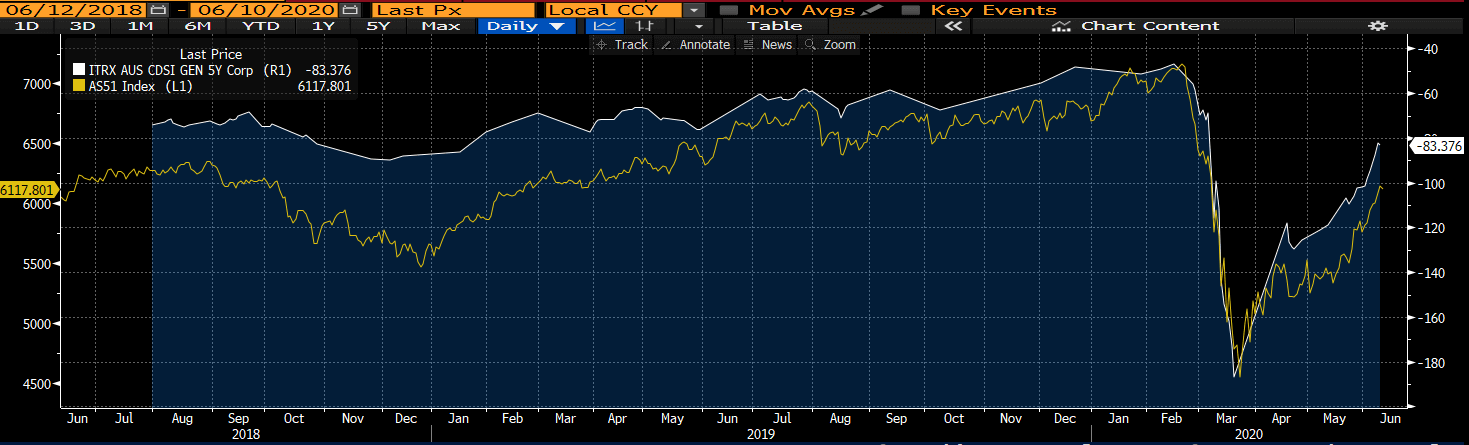

The recent healthcare crisis is no different, with credit bonds represented by the Australian Itraxx (Credit Default Swap index) price versus the ASX 200 index.

Yellow = ASX 200, White = Aus iTraxx

Source: Bloomberg

Credit market opportunities

Because of this relationship change – credit markets are currently disjointed and may return to trading like pure fixed income securities (based upon interest rates) rather than equities (based upon earnings) in the present to neat future.

With this comes the opportunity that selective credit bonds that aren’t at likely to experience repayment risk – selective A and BBB-rated issuers – and thus potentially about to see capital price appreciation.

I take note of the below RBA chart released last week, showing the sell-off in credit bonds over Q2 2020, breaking the longer-term trend of credit bond market appreciation.

Once the current crisis is ameliorated, we may likely see the index as a whole mean-revert to its long-term trend reflecting low interest rates reducing credit risks through lower costs of funding business operations.

However, in the meantime, we are starting to see selective credits with entrenched market share rallying through central bank explicit and implicit support, and investor confidence returning.

Selective opportunities

We remain cautious of viewing credit bonds as an overall market – there are idiosyncratic risks that are missed when looking at credit as an asset allocation or in buying credit bonds as a basket.

Being selective in viewing opportunities is important now more than ever, as earnings and profitability and the long-term survival of corporate bond issuers has been tinged with uncertainty.

Entrenched market share, stable earnings and capitalisation remain key, and there is a natural attrition towards bonds that reflect this view right now, as we rotate holdings from lower investment-grade securities to those more highly rated – as long as the ratings reflect the above characteristics.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.